{kind=link}

Should You Sell Your House Before Your Mortgage Renewal in Winnipeg?

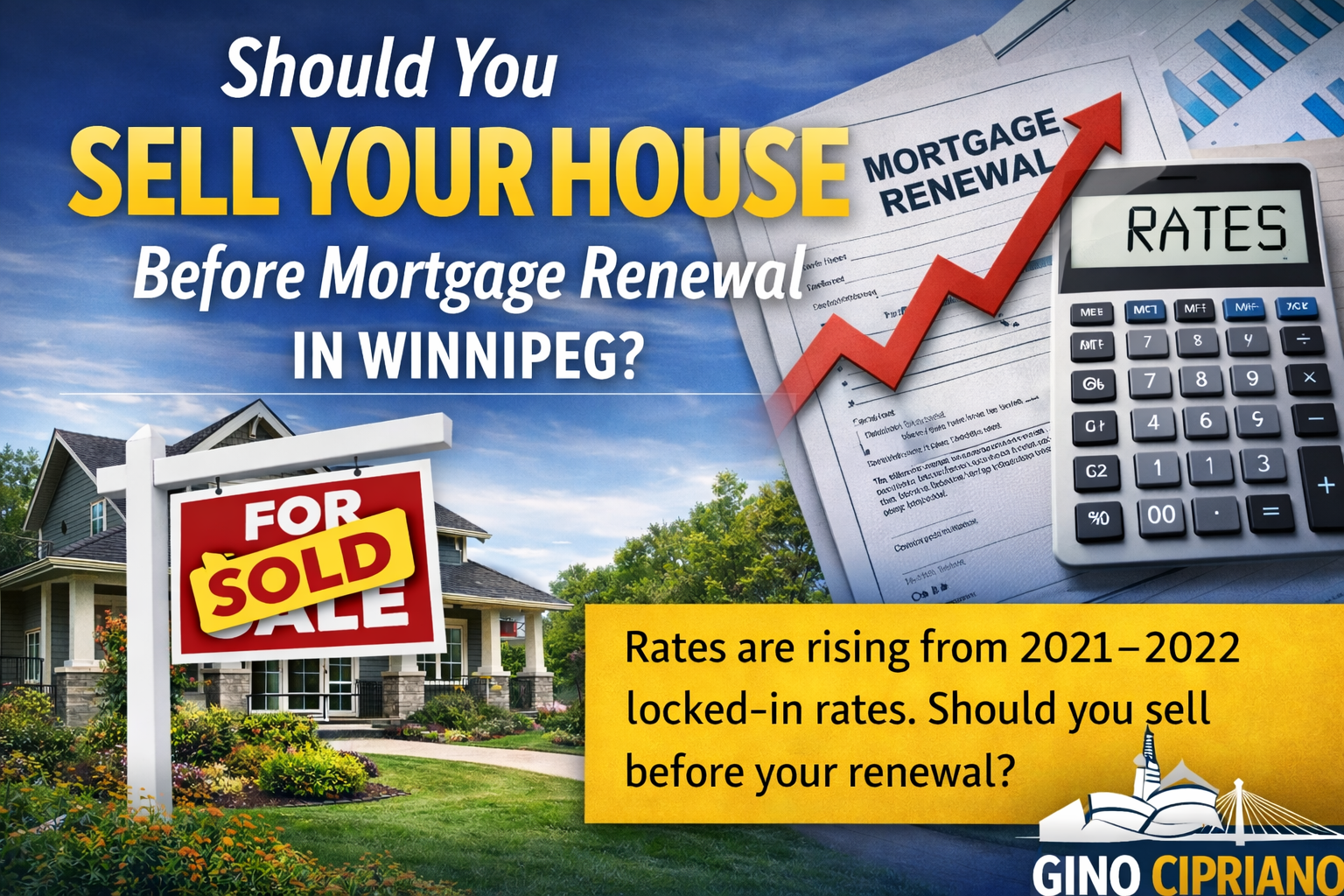

Many Winnipeg homeowners locked into historically low mortgage rates in 2021 and 2022. As those terms expire, renewal rates in 2026 are significantly higher — and for some homeowners, the payment shock is real.

If your mortgage renewal is approaching, you may be wondering whether it makes sense to sell your house before locking into a higher rate. This guide breaks down when selling before renewal might be a smart move — and when it might not.

Why Mortgage Renewals in 2026 Are a Bigger Deal

During 2021 and 2022, fixed mortgage rates were often under 2%. Today, renewal rates are substantially higher. For many homeowners, this means:

- Higher monthly payments

- Reduced affordability

- Less flexibility in household budgets

- More difficulty qualifying under current stress-test rules

Even if you’ve been managing your mortgage comfortably, renewal can force a financial reset.

When Selling Before Renewal Makes Sense

Selling your home before renewing your mortgage can be a strategic decision in certain situations:

- Your renewal payment would significantly strain cash flow

- You’re planning to downsize or relocate anyway

- You’ve built strong equity and want to preserve it

- You’re concerned about long-term affordability at higher rates

In some cases, selling before renewal allows homeowners to exit on their own terms rather than being forced into tough financial decisions later.

Why Timing Matters in Winnipeg

Winnipeg’s real estate market behaves differently than larger Canadian cities. Pricing, demand, and buyer competition can vary by neighbourhood and season.

Selling before your renewal date gives you:

- More flexibility in pricing and timing

- Less pressure to accept unfavourable renewal terms

- Time to prepare and present your home properly

Waiting until after renewal can limit options — especially if higher payments begin to impact your finances.

What About Penalties for Selling Early?

Many homeowners worry about mortgage break penalties. While penalties do exist, they are often smaller than expected — especially for fixed-rate mortgages nearing the end of their term.

When comparing options, it’s important to weigh:

- The cost of mortgage penalties

- Higher monthly payments over the next 3–5 years

- The opportunity cost of staying in a home that no longer fits your budget

In many cases, selling before renewal can still make financial sense even after penalties are considered.

When It Might Make Sense to Stay

Selling before renewal isn’t right for everyone. You may choose to stay if:

- Your income comfortably supports the new payment

- You plan to stay long-term and ride out rate cycles

- Your home no longer fits market demand for selling

This is why a personalized analysis is critical — not blanket advice.

Get a Clear Plan Before You Decide

Before renewing or listing, homeowners should understand exactly what their options look like. A clear plan includes:

- Your expected renewal payment

- Your home’s current market value

- Estimated selling costs and penalties

- Alternative housing options if you sell

With the right information, you can decide whether selling before your mortgage renewal is a smart financial move — or whether staying put makes more sense.

Final Thoughts

For Winnipeg homeowners coming off 2021–2022 mortgage rates, renewal can be a turning point. Selling before renewal isn’t about panic — it’s about control, planning, and protecting your financial future.

If your mortgage renewal is coming up and you want an honest, no-pressure analysis of your options, reach out anytime. Knowing your numbers early gives you leverage — and peace of mind.